Key takeaways

- Global supply chains remain under immense pressure and will remain a challenge going into the fast-approaching holiday season.

- Demand for goods remains supercharged from several factors including unprecedented fiscal and monetary stimulus, re-opening, growing confidence and a shift in consumer spending patterns.

- The supply-demand imbalance is putting intense pressure on industrial vacancy, which is at an all-time low, as well as rents, which are growing at a rate that more than doubles the rate of inflation.

- Labor shortages and lack of building materials are constraining the supply pipeline—creating even more upward pressure on rents going into 2022.

- The supply chain issues are directly linked to the disruption caused by the pandemic; as the pandemic recedes, these issues will begin to resolve.

- Supply constraints will not derail the industrial sector’s momentum, which is in midst of the single greatest boom ever observed.

The disruption

Fundamentally, this is an issue of supply and demand. The demand narrative is straightforward. Spending is increasing because labor markets are improving, wages are growing, and households have pent-up spending power, partly due to the enormous fiscal stimulus passed by the government. Inflation has been increasing across the developed world, but it has increased more in the U.S. where fiscal stimulus has been largest. Add to that a shift in spending patterns that favor goods over services—a trend that has further exacerbated supply-demand imbalances. Looking forward, however, many of these demand-side forces should fade rather quickly. The initial burst of activity after reopening has passed. The effect of higher savings on spending will decrease over time once households reach their preferred savings levels, and households only need so many hard goods like cars, ovens and furniture.

The supply side of the economy is really where the issue lies. COVID-19 is the main reason for that. In short, manufacturers and distributors still face substantial challenges ensuring sufficient supplies of goods are available due to worker shortages (truck drivers, port workers, warehouse pickers, etc.), health concerns, a lack of key components (shipping containers) and raw materials (such as semi-conductors). Perhaps of greatest note is that this is now a global issue. At the height of the pandemic and as Europe and the U.S. were entering lockdown, Greater China was exiting lockdown and able to fill the manufacturing void. However, with practically all economies reopening, shortages of raw materials and back-logged supply chains are now global. There are a range of local issues exacerbating these conditions, including adverse weather events, union strikes and the blocking of the Suez Canal by the EverGiven.

Fundamentally, these disruptions are resulting in demand exceeding supply and therefore strong inflationary pressure. According to Moody’s Analytics, Producer Price Inflation is trending above 10% year-over-year (YOY), while shipping costs have increased by as much as 400% YOY, reflecting the difficulty in moving goods around the world. The same forces driving economic demand and inflation are supporting industrial warehouse demand (in many cases as unprecedented levels) and thus, driving rent growth across the globe.

How the disruption is impacting the industrial real estate sector

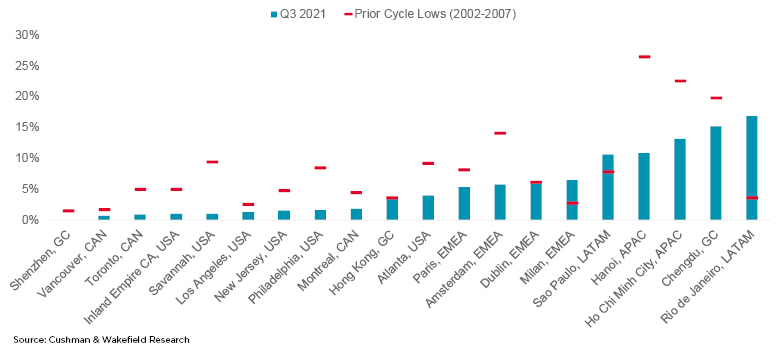

The impacts on industrial real estate have been extensive across the globe in all property types highlighted by vacancy rates at record lows in many markets and soaring asking rents, especially in the U.S. and parts of Europe. For example, the current vacancy rate in U.S. port cities such as Los Angeles, Savannah and New Jersey are under 2%. In London, the current level of availability has fallen by 33% in just 18 months from March 2020 to September 2021. London rents have grown 23% in the same timeframe while in the third quarter of 2021, U.S. rent growth surged to 8.3% YOY. Beijing warehouse space is sitting around 1.7% and has been tight for several years. Shenzhen is seeing warehouse space sitting at less than 1% at mid-year. These trends are being driven by record levels of demand for warehousing space across markets in Europe, North America and Asia Pacific.

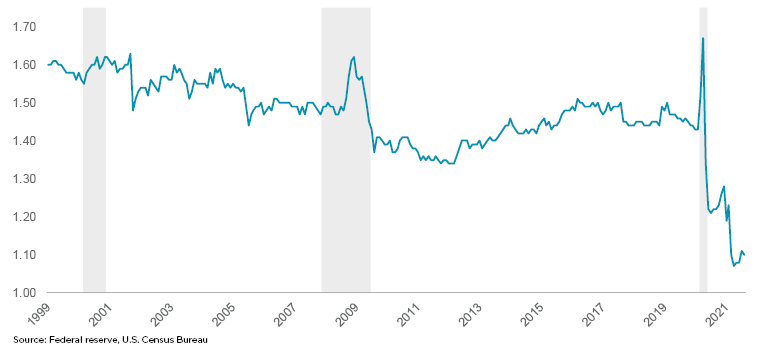

In part, demand has been fuelled by the acceleration of e-commerce, and while e-commerce isn’t a new phenomenon, transaction levels have dramatically increased as consumers have preferred to, or been forced to, purchase goods online rather than in-store. And, the average consumer is purchasing more goods in general! This is especially true in the U.S., which had a slower initial e-commerce adoption compared to Europe and Asia. Prior to the pandemic, e-commerce sales accounted for 17.9% of global retail sales according to Digital Commerce 360. It jumped to 20% during the peak of the pandemic in December 2020 and today it sits at 19.5% according to Statista. From there, it is expected to grow. This major shift to online sales has driven the need for more logistics space to store and distribute goods to end-users, which includes more than just shipping to a mall or store location, further fuelling demand for “last-mile” sites. Beyond this, the pandemic has revealed the fragility of just-in-time inventory management, leading many producers to shift to holding a greater amount of “safety stock” and transitioning to “just-in-case” inventory management, further driving demand for warehousing space. In May, the U.S. saw the retail industry’s inventory-to-sales ratio reached 1.04, meaning there was just over a month’s worth of inventory available, an all-time low (with data dating back to 1980). The most recent August numbers are not much higher at 1.07, due to the constant demand for online goods. Some good news is that other segments of the U.S. supply chain (such as manufacturers and wholesalers) do not have historic lows for their respective sector.

Developers have been ramping up development over the past several years but have been conservative (relative to the last expansion) on speculative development particularly due to the lessons learned after the global financial crisis and the overhang of space that took years to absorb. As an example, the United States has seen build-to-suit rates at about 30%-40% as a percent of total development under construction in the current expansion compared to 10%-20% at the height of the last expansion. This is not to say that speculative development is not happening, or that there isn’t an appetite for it. Developers prefer to operate on a “build-to-suit” basis based on needs of occupiers with regard to location and asset customization.

It can also be difficult to upgrade existing real estate assets. Occupiers are often looking for higher clear heights, better automation, and higher quality amenities for the workforce. This can be a challenge in today’s market, especially when, in the U.S. alone, 70% of industrial inventory was built before 2000. Others are considering retrofitting or refurbishing—sometimes taking buildings all the way back to frame—older warehouses to provide additional options in the particularly supply-constrained markets or infill markets.

Of course, the largest constraints on the supply side are related to the pandemic itself. Materials shortages due to shipping/port congestion issues have become a major challenge across most of the globe. Container shipping costs from China to U.S.’ West Coast ports reached a new high of more than $20,000 per 40-foot container in 2021 (compared to roughly $2,500 per container, pre-COVID-19). These increases are partially due to rising COVID-19 cases across the globe, slowing the rate of container turnaround time and leading to bottlenecks of container storage and challenges moving goods on and off ports. This means that, as well as driving shipping costs higher, ships are sitting outside of the ports for extended periods of time (nearly at peak 2020 times of two weeks compared to a day or two tops pre-COVID-19). So, even as production levels of building materials have increased in other countries, getting the inventory out into the markets where they are needed and at the pace they are needed is challenging. This is a serious impediment to getting supplies on time, as shipping and logistics companies carry 90% of world trade and are causing longer than usual lead times for building supplies needed to construct new real estate at a time when the construction pipeline is at record levels. Steel, pre-cast concrete and lumber prices remain high which is also impacting construction delivery.

In addition to the raw materials issue, labor shortages have also been an ongoing challenge throughout the pandemic which is slowing industrial supply. In the U.S., according to the U.S. Bureau of Labor Statistics, there are 10.4 million total job openings as of September 2021: 333,000 in the construction industry, 897,000 in the manufacturing industry and 589,000 in transportation, warehousing, and utilities. The U.S. labor force participation rate plunged from 63.3% pre-pandemic to 60.2% in April 2020 and has been very slow to climb back. As of October 2021, it stood at just 61.6%. Surveys show the primary reasons for not returning to work are largely due to the pandemic (i.e., either sick or caring for the sick, childcare, or company went out of business during the pandemic). The pandemic-related labor issues echo throughout the global markets as well. In South East Asia, labor has vacated high-density, high-virus caseload cities to wait out the pandemic in more rural homelands. In Europe, the challenge is particularly acute in key distribution roles such as truck and forklift drivers and skilled technicians. Impediments to the movement of labor, either as a result of COVID-19 or political disruption such as BREXIT, have been identified as a significant factor. It will take an easing of the pandemic and a return to ease of moving across international borders before labor supply will begin to normalize. Longer term, structural changes to labor through population aging and a general upskilling of the labor force are also likely to drive wider supply chain redesign and optimization, leading to ongoing changes in demand for assets at the local level.

When will the supply chain issues resolve?

In September, Moody’s Analytics’ supply chain stress index was nearly 40% above its Q4 2019 level and significantly higher than any period since 2010. Since then, new coronavirus infections have generally trended lower globally and vaccinations have trended higher. As of November 2021, over 50% of the world’s population over the age of 12 had been fully vaccinated. In much of the developed world, the percentages are well above 80%. The situation remains fluid, but in general, the supply chain challenges are tethered to the trajectory of the pandemic itself. As we move toward the end of 2021, and as the pandemic becomes less threatening, we note that ports are reopening, stay at home orders are being lifted and moving across borders is becoming less restricted. Assuming no virus setbacks at this stage, it is generally assumed that the supply side of the economy will kick into full gear in 2022 and most of the supply chain issues will start to moderate towards the end of 2022. Likewise, some of the supply of labor issues are also largely linked to the pandemic, so this too should start to improve over the coming quarters.

What can we do about it?

Occupiers

- Cost Options: Net asking rents are increasing significantly and swiftly in the majority of global industrial markets, and there are new cost factors like building costs, land values and planning costs that are putting even more upward pressure on rents for at least the short term. Consider secondary markets with untapped labor pools. Rents, for the most part, are only about 5%-8% of costs, so paying a higher rent to secure more labor options and lowering costs may be a good play.

- Identify largest issues: By identifying the most acute issues in supply chain, occupiers will be able to target the greatest needs in their supply chains to perform at the strongest capacity. By looking to where there may be a bit of space capacity, or unnecessary locations or even consolidating operations in some locations while expanding in others, will be key for optimization.

- Plan for the future: Logistics and industrial real estate supply is constrained in many markets which means the ability to secure buildings where and when needed is ever more challenging. Occupiers need to look to the future of their business when selecting sites to optimize supply chains. Also, when planning to renew your lease or search for new space, don’t wait—the constraints in the market are likely to persist for at least the short term.

Investors / developers

- Land is key: Investors/developers with land positions have an opportunity to create product in an environment of strong demand and rising rents. The risk here is that it may be difficult in the near-term to secure building materials and labor, which will be at higher prices than in the recent past. It is crucial to place orders well in advance to secure materials to avoid the risk of not being able to complete buildings on time.

- Understanding the value of the building: In terms of occupiers, if the building isn’t crucial to their supply chain or up to the standard of the user, an increase in rent may not be worthwhile for them. It is a landlord-favored market across the globe, but if there are unreasonable terms (lack of TIs, escalations or extremely high rents), tenants might seek opportunities elsewhere.

- Partnering for long-term success: By working with occupiers to understand their needs, investors and developers position themselves by securing the most desirable lease options. Continuing to ask tenants what matters to them will help development down the line and provide the ability to push a higher rent for better quality space and securing higher credit tenants.