The rise of technology and seismic demographic shifts may impact the finance technology world

Fintech has been around for decades, and while it isn’t anything new, the relationship with the traditional banking system has moved from being largely symbiotic to increasingly disruptive and competitive.

Looking towards the future, there is potential for this disruption to be turbo-charged. Three fundamental reasons are driving this shift: seismic demographic change, a burgeoning middle class and further digitalization of financial services.

From Symbiotic to Competitive

The global fintech industry has grown significantly, with estimates suggesting that more than $70 billion in venture capital has been raised to support the industry in the past two years alone.1 This trend is expected to continue with forecasts of growth ranging from eight percent to more than 20 percent per annum by 2025. The pace of technological development, the willingness to fund that development and the rapid adoption of this technology, especially by younger generations, have been key drivers.

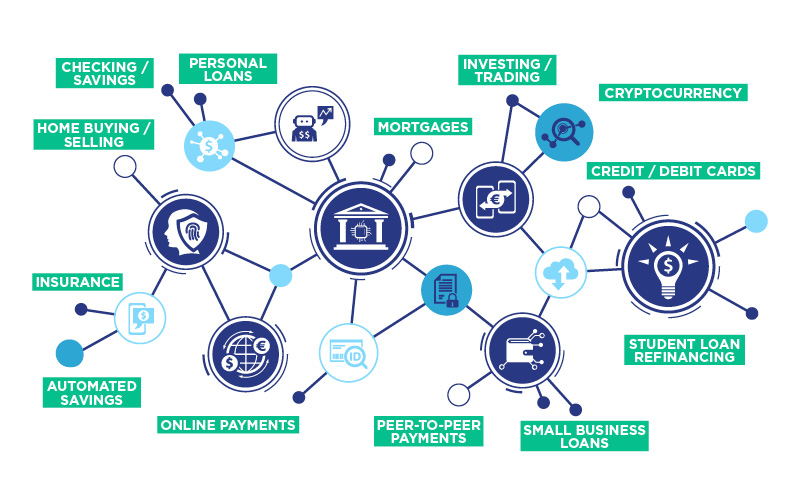

Fintech has evolved from complementing existing services offered by banks, such as ATMs and online banking, to a situation where they are in direct competition with one another. For example, the fintech sector surpassed traditional banks' global share of unsecured loans in 2015, and was the leading source of personal loans in the U.S. in 2018. As a result, banks are starting to feel increased pressure on services such as payments, checking, savings, lending and investment management.

Unfortunately for banks, it doesn’t stop there. For many, when thinking about fintech, the likes of Apple, Google, Amazon, PayPal or even peer-to-peer payment transfer platforms such as Venmo come to mind. While these are high-profile companies with huge user-bases, there are other lesser known giants in the fintech world, with many focusing on third-party payment platforms. These include Ant Financial, originating from Alipay (part of the Alibaba group), which is valued at around $150 billion, as well as Adyen and Stripe. In addition, eight new fintech unicorns were created in the past six months alone. It is becoming clear the market is more competitive than ever before.

Seismic Demographic Shifts

While the rise of technology has been part of the story, seismic demographic and cultural shifts have also played a role, none more so than the rise of Millennials. The generation born between 1980-1995 have collectively had a profound impact on society, bringing with them a thirst for technology, immediate gratification, flexibility, authenticity and transparency. Their impact on the financial sector goes beyond this as they make up about 40 percent of the world’s working population. As their spending power increases, they are becoming even more influential consumers.

While the majority of Millennials have visited a bank, they are predominantly mobile-oriented, with around 94% actively using online banking services. Read our report Demographic Shifts: The World in 2030 for more analysis on the ways Millennials, Gen Z and Baby Boomers are all changing the future of commercial real estate.

They use online banking services regularly at a rate three times that of older generations. These statistics, combined with the increased use of contactless payment methods and a declining reliance on cash, have been key considerations in the rationalization of retail bank branch and ATM networks over much of the western world. England has been especially hard hit know as an estimated 30 percent of bank branches have shuttered in the past three years.

It remains to be seen whether the effects of COVID-19 will further accelerate this trend, though early reports suggest that as social distancing has become more universally adopted, there has been strong growth in digital financial services.

To compound matters, nearly half of Millennials do not think their bank communicates to them through the right channels. Consequently, this generation has little affinity to existing bank brands. Among those surveyed, 73 percent of Millennials said they would be more receptive to financial services from tech companies such as Google, Apple and PayPal than their current bank.

Additionally, 33% believe that banks will not exist within five years.

While that may be overly pessimistic, it does point to Millennials’ lesser loyalty to traditional banking service providers.

Hot on the heels of Millennials is Gen Z, born between 1996-2012. While they are still in the early days of their banking experience and professional careers, there are already some indicators of their intent. This is the first generation exclusively born into the digital age, making them more tech-savvy, but also more cautious about money having grown up during the 2008 Global Financial Crisis.

As a result, they tend to gravitate to brands they know, trust and that provide them with a highly personalized experience, which is likely to be increasingly found in the digital world. In support of this, Morgan Stanley research estimates that 50 percent to 80 percent of smartphone-owning members of Gen Z are already using mobile banking. However, they are far from a homogenous generation with a UK study finding that 45 percent of Gen Z would not open an account with an online-only bank (the other 55 percent would use an online-only bank). The majority of these respondents cited a lack of physical presence as a key reason. This underlines their more cautious approach to finance as well as the “phigital lens” that Gen Z brings – the experience that all of life is both physical and digital.

Just as retailers with both physical stores and eCommerce capabilities have thrived over the past few years, fintech and traditional banks will need to respond accordingly and focus on customers’ digital and physical needs.

Asia Pacific and the Rise of the Super-App

For a look at what could be next, attention turns to Asia Pacific, the latest hotbed of fintech activity. Over the past two years, Asia Pacific has accounted for 40 percent, around $30 billion, of fintech venture capital raised – broadly on par with the 42 percent invested in North America.8 At the national level, it also has some of the highest adoption rates with penetration in China and India nearing 90 percent. By comparison, the UK’s adoption rate is 71 percent and the U.S. is just 46 percent, according to EY's Global FinTech Adoption Index. There is no doubt the globally leading levels of smartphone usage in China and India are playing a role. As a result, we see a more holistic adoption of fintech than perhaps seen in other geographic regions.

Couple this with the world’s largest share of Millennial and Gen Z populations along with a burgeoning middle class and it is little wonder that fintech firms have such a focus on the Asia Pacific region.

What may be surprising though is that a large proportion of the region is still either unbanked or underbanked – i.e., they have no bank account or seldom use it. The World Bank estimates that two-thirds of Indonesia’s population is unbanked, while half of India’s bank accounts are inactive. Both of these countries offer great potential for fintech with their sizeable populations, increasing wealth and lack of relation to any existing financial organizations. For these reasons, Asia Pacific has seen the rise of the “super-app.”

In simple terms, a super-app is many apps under an umbrella app or an “all-in-one” experience. It is a predominantly Asian and, more specifically, South East Asian phenomenon. Within fintech circles, Grab is considered a leader. What started as a ridesharing app in Malaysia in 2012, has quickly grown to become a behemoth in the South East Asia region. Grab is active in 196 cities across eight countries and has extended its services; offering a wider range of ride-hailing services, delivery services and — more importantly in this context – fintech. Through three subsidiaries – Grab Financial, GrabPay and GrabRewards — services such as lending, insurance, peer-to-peer fund transfers and South East Asia’s largest loyalty program are now part of its arsenal.

Through its lending services, Grab is already directly targeting business customers using its payment platforms to help them expand. Targeting SMEs, loans are typically small, but numerous given Grab’s geographic coverage. Interest in these loans is fueled by low-interest rates, no requirement for security deposits and fast approval times – three factors that traditional banks often cannot deliver simultaneously. While there may seem to be an elevated risk in this type offending, Grab already has insights into the business through the cash flow from its payment platform and can see levels and variability in trade, thereby helping to mitigate their lending risk.

We see a similar situation replicated at the individual level. The high-level of mobile smartphone penetration represents opportunity. Initial exposure to the brand is often through basic services such as ridesharing or food delivery, all paid for through the payment platform. It is then not a large step for this customer base to use peer-to-peer money transfer and seek higher-level financial services such as lending and insurance. All the while, discounts and offers are available across other services offered by the app as a reward for this loyalty. Indeed, 60 percent of fintech adopters prefer to view all their financial products through a single platform.

The unbanked are also more likely to turn to these types of financial instruments as they seemingly have a greater level of trust. What takes days and requires significant paperwork in a traditional bank can be achieved in minutes online. Tie this with the growth prospects in the region and it is easy to understand how many Asian fintech companies are commanding such high valuations.

What’s Next

Asia Pacific is now considered the global leader in fintech having developed rapidly in recent years, but it is on the cusp of being turbo-charged. The combination of high demand for mobile services together with large, young and increasingly wealthy populations makes the financial system ripe for continued disruption.

It is almost certain that the sector will continue to grow and evolve at a rapid pace across the region, with fintech dipping into more complex financial services that have traditionally remained the remit of the incumbent banks. In the future, there is potential that we will see a return to a somewhat more collaborative approach between banks and fintech – the former bringing the physical experience while the latter focuses on the digital experience – to fully address the user requirements of younger generations. With Asian fintech paving the way, it is only a matter of time before the U.S. and Europe follow suit.

* All currency amounts listed in USD