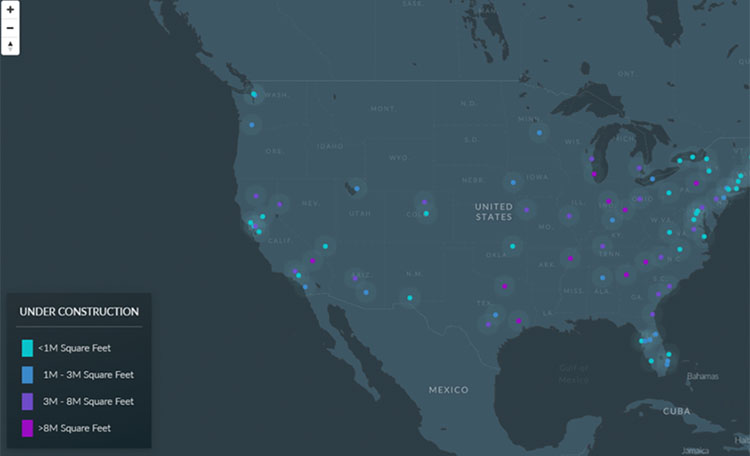

The U.S. industrial construction sector has seen a slowdown after delivering 1.1 bsf of new space in 2022-23, with speculative development previously driving construction due to pandemic-induced demand. The Midwest experienced a surge in speculative deliveries, totaling 166 msf across major markets and 334 msf since 2018, with over 70% occupancy by Q1 2024. However, economic challenges have dampened demand, leading to increased vacancy rates and a 40% reduction in the construction pipeline YOY, signaling a continued decline in 2024. Speculative construction starts in the Midwest have also fallen from an annual average of 140 to just 92 by Q1 2024. The data tells us that while the industrial boom is slowing, the Midwest remains resilient.

The Midwest Speculative Construction Report analyzes speculative with buildings that are 100,000 sf and greater, a clear height of 28’ and greater and built since 2018, in Chicago, Indianapolis, Cincinnati, Columbus, Kansas City, St. Louis, Minneapolis, Detroit and Louisville. Specifically, each market takes a deep dive into:

- Speculative bulk occupancy

- Number of buildings completed

- Square feet delivered

- Average building size

- Number of developers involved

- Number of current tenants